ALRAQABA . ISSUE 15

49

First: Audit Reporting Standards:

Different Supreme Audit Institutions (SAIs) produce various reports in accordance with the INTOSAI

standards; including financial audit reports, performance audit reports, and compliance audit

reports, as discussed below:

Financial audit reports:

The financial audit reports are issued by SAIs as a result of auditing a comprehensive set of

financial statements. Those general purpose statements shall be prepared in compliance with

the financial reporting framework, which is intended to achieve a fair presentation of financial

statements and provide guidance on the matters to be examined by an external auditor to form an

opinion on those statements. When preparing financial reports, it is imperative that the auditor takes

into account the fundamental distinctions between the requirements of the INTOSAI Standards

for Supreme Audit Institutions (ISSAIs) and the International Standards on Auditing (ISAs). Those

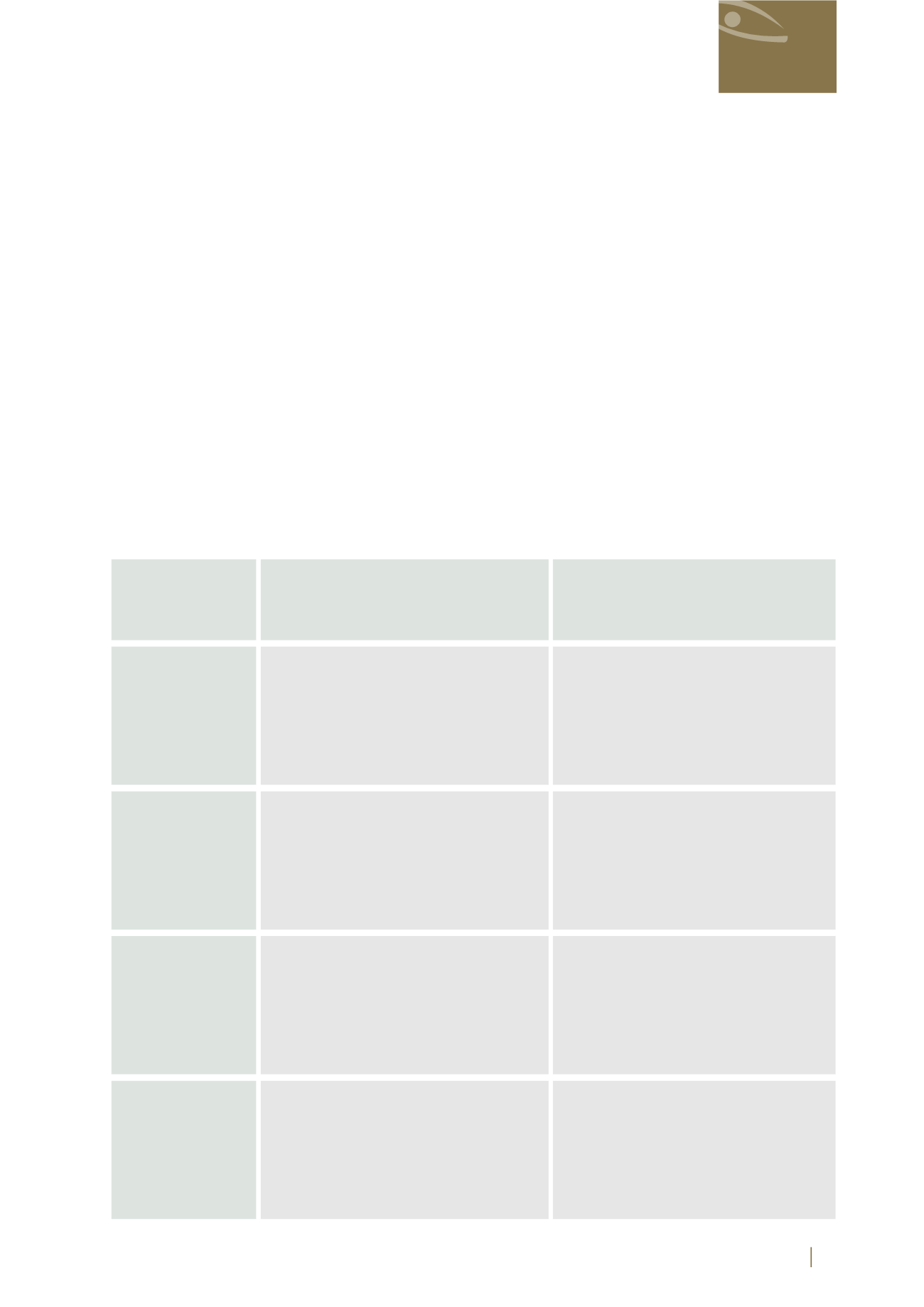

distinct differences are summarized in the following table:

Forming an Opinion and Reporting

on Financial Statements

(ISSAI 1700)

Modifications to the Opinion in the

Independent Auditor’s Report

(ISSAI 1705)

NA

The Emphasis of Matter Paragraphs

and Other Matter Paragraphs in the

Independent Auditor’s Report

(ISSAI 1706)

Forming an Opinion and Reporting

on Financial Statements

(ISA 700)

Modifications to the Opinion in the

Independent Auditor’s Report

(ISA 705)

Communicating Key Audit Matters in

the Independent Auditor’s Report

(ISA 701)

The Emphasis of Matter Paragraphs

and Other Matter Paragraphs in the

Independent Auditor’s Report

(ISA 706)

Forming an

opinion

Modifications to

the opinion

Communicating

key matters

“Emphasis of

Matter” paragraph

and “Other

Matters” paragraph

Aspect

ISSAIs

ISAs

Audit

Finance and