ALRAQABA . ISSUE 15

63

the nature of the company’s activity; developing

the audit plan and determining the audit tasks

for each member of the team; determining the

timeline and the number of auditors responsible

for carrying out the defined audit tasks; and

4.

identifying the internal and external difficulties

that an auditor may face in the company.

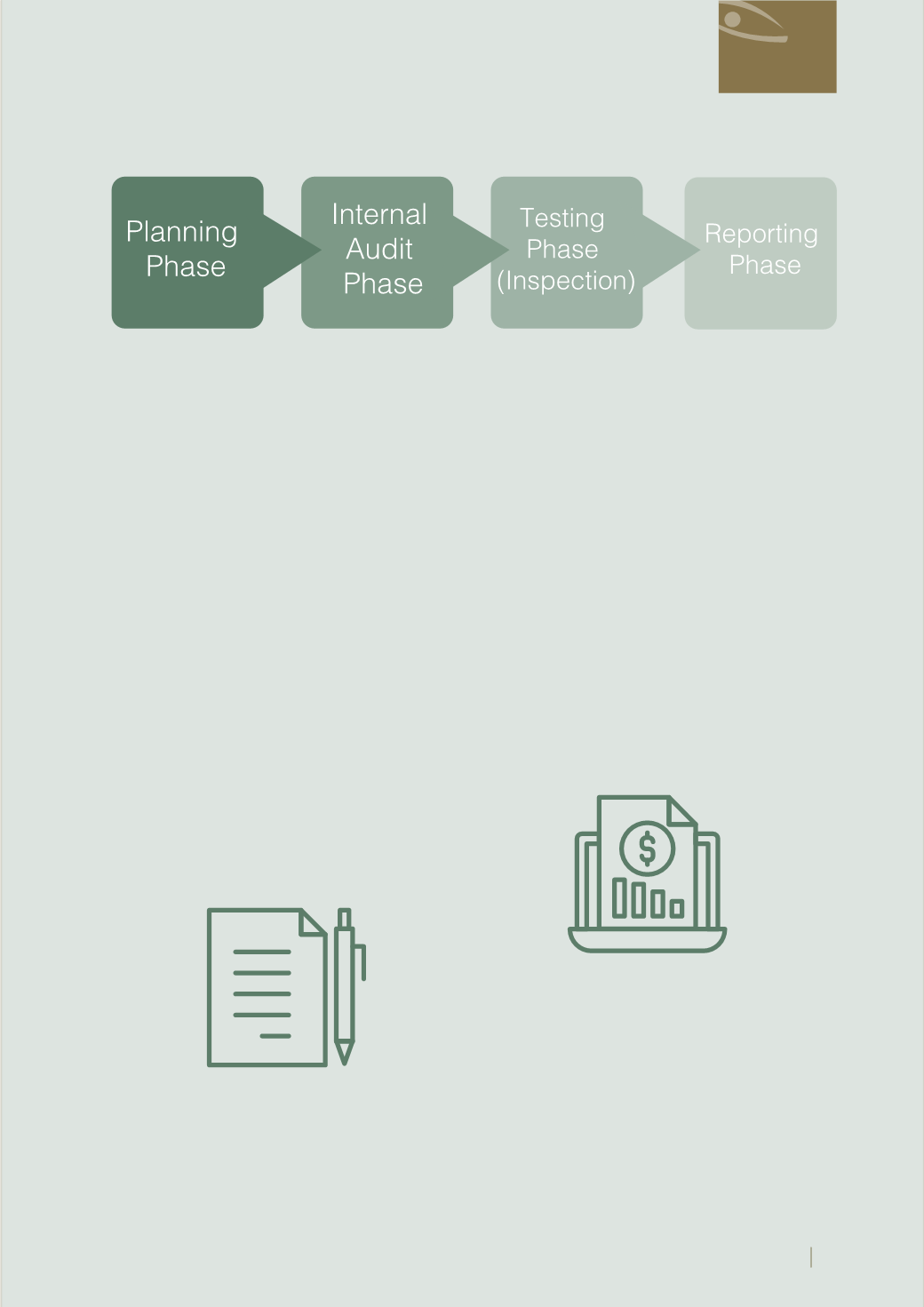

Second:

Internal Audit Phase

Having robust internal audit systems is vital

for ensuring the soundness of a company’s

business. It would also contribute to enhancing

trust and help to understand the stages under

which financial transactions are processed,

starting from phase one to the phase of

reporting. In addition, having efficient and

effective internal audit systems in a company

would facilitate the audit process and

considerably save time for SAB auditors in

carrying out their audit functions.

Third: Testing Phase (Inspection)

The accounting system consists of a range

of processes pertaining to the recording of

accounting data at the company level and the

preparation of final statements and accounts.

Those processes are subject to a specific

framework of foundations, rules, terminology,

and definitions in order to serve certain

objectives.

Further, the accounting system entails that the

company commits to maintaining the books and

records based on its size and activities, along

with providing the data required by the system.

In general, the components of an accounting

system are the financial accounts (which

are documents on financial transactions),

accounting classification (i.e., accounting

manual), books and records (i.e., journals and

ledgers), and interconnection/ relationships

between components (accounting system

instructions).

Audit proof of evidence and the means to

obtain such evidence:

It is necessary to obtain evidence for data

included in the financial statements in order for

the auditor to reasonably draw his/her opinion

on the validity of the presented data. There is

a range of methods that the auditor could use

in collecting information and obtaining proof of

Publications